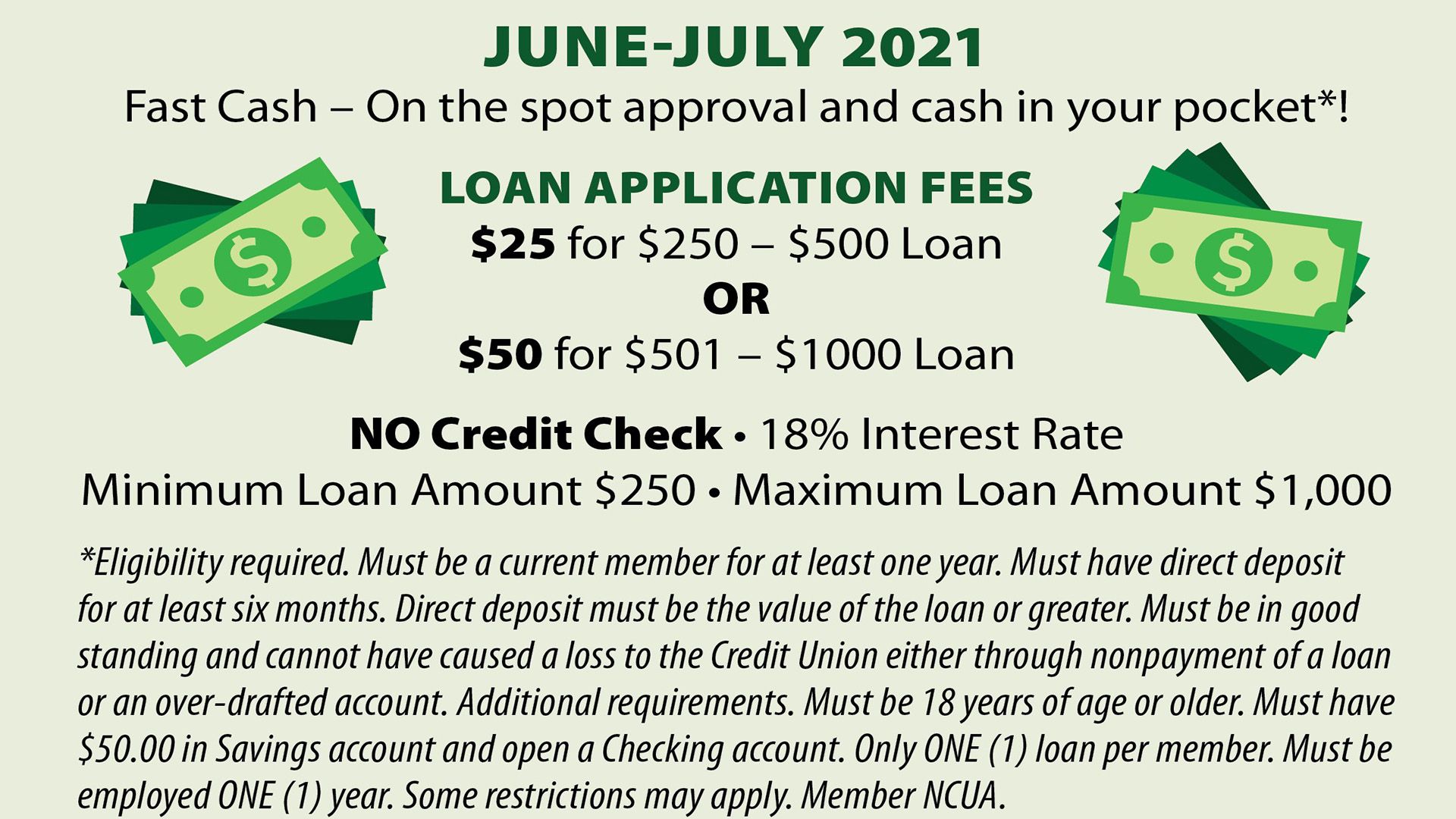

Discovering a down payment to possess a property tends to make perhaps the most devoted saver earthquake within their sneakers – it’s an enormous amount away from transform.

Incase your plunk down less than an excellent 20% deposit, you can build more money in the way of private mortgage insurance policies (PMI).

Very, what is actually PMI, how much does it rates, and exactly how do you make money? We’ll mention all those responses and even talk about implies you could end PMI.

Continue reading to know about things PMI (if in case your mind is spinning of every home loan acronyms we’ve an effective homebuyer’s self-help guide to decoding financial acronyms to aid there, too!).

What exactly is PMI?

Simply speaking, PMI is a kind of insurance coverage one to protects your own lender in the event that your standard on the financing. The lender are likely to perhaps you have build PMI repayments for folks who cannot build a down-payment greater than otherwise equivalent so you’re able to 20% of your own loan amount.

Such as for instance, can you imagine your borrow $150,one hundred thousand purchasing a property. You will need to make a beneficial $31,100 down payment to prevent PMI.

PMI merely pertains to old-fashioned money, otherwise financing maybe not supported by the You.S. authorities. You https://paydayloanalabama.com/auburn/ have got heard of other kinds of financial insurance coverage instance because the home loan premium (MIP) to have FHA loans but MIP isn’t the identical to PMI.

Loan providers generally speaking enables you to request that PMI getting terminated in the 80% dominant mortgage equilibrium the point where your home is located at 20% collateral. Or even consult a cancellation, their bank is necessary for legal reasons to eliminate they in case the dominating financing balance is located at 78% of your fresh property value your property.

But there are even other kinds of PMI that don’t succeed you to discontinue money slightly thus without difficulty. We will look closer during the those people products less than.

PMI just relates to old-fashioned money. If you get a traditional financing, you might choose from home loan systems, also a changeable-rate mortgage (ARM) and a predetermined-rates financial.

With an arm, you I given that interest rate can move up otherwise off centered on industry conditions, making it riskier. The rate for fixed-price mortgage loans, at the same time, remains a similar.

There was factual statements about your own PMI money in your Mortgage Guess and Closing Revelation, a couple of files you to definitely reveal all the info about your home loan.

Different kinds of PMI

- Borrower-paid down home loan insurance (BPMI): The preferred kind of PMI, BPMI happens when your the newest debtor pay for mortgage insurance coverage.

- Lender-repaid mortgage insurance rates (LPMI): Their financial I to you personally for the a lump sum after you romantic on the loan. In exchange for LPMI, your accept a higher rate of interest on your own home loan. not, it is very important remember that if you deal with LPMI, you cannot cure it. The only method you could switch it pertains to refinancing the home loan.

- Single-premium mortgage insurance coverage (SPMI): SPMI enables you to pay your home loan insurance in one single swelling sum, getting rid of new payment per month requisite. However, just remember that , it is nonrefundable for individuals who promote your house shortly after but a few ages, you simply cannot have that money back.

- Split-superior financial insurance coverage: Split-premium financial insurance coverage takes a hybrid approach to BPMI and you will SPMI. You might will spend part of the PMI in a great lump sum payment while making money as well. You’re capable of getting a refund in case your home loan insurance is canceled.

How can i Create PMI Repayments?

The lender I. Widely known treatment for purchase PMI relates to going the payments into the month-to-month homeloan payment. Your PMI repayments usually are kept into the a keen escrow account, a 3rd-party membership and that holds fund temporarily up until owed. Your loan servicer, which features the mortgage when you found it from your lender, ensures that your PMI repayments will go into compatible creditor punctually.??

It is possible to make a lump sum on a yearly basis. You will also have the option and then make a single fee courtesy single-premium mortgage insurance otherwise love to create a limited upfront payment courtesy split up-superior mortgage insurance rates.

How to avoid PMI

However, whenever that isn’t possible, keep in mind that you could potentially demand that the financial terminate PMI when you get to 20% security of your property. Many residents do this by simply making even more costs or and also make domestic developments that enhance their residence’s worthy of, for example. Almost every other conditions set by your lender may include:

- Acquiring yet another appraisal.

- And also make your mortgage repayments on time.

- Composing a page towards the bank stating that you want PMI got rid of.

Discover more about PMI

When buying property, it is possible to easily know that and work out a down-payment from 20% may possibly not be the best complement your position.

You are expected to get PMI if that’s the case, nevertheless commonly end when you struck 78% of your own financing to help you value proportion (LTV). LTV are going to be calculated by the picking out the difference between the loan count plus the market value of your house.

The bottom line is one to PMI will eventually help the rates of one’s mortgage. It doesn’t manage you, sometimes – it handles your own lender on the risk they undertakes whenever loaning to you.

But you’ll find different kinds of PMI for assorted affairs, so be sure to do your research before choosing suitable to you personally. Generate Morty your own go-so you can to own recommendations on to make PMI costs and how to end PMI completely. We will make it easier to each step of method.